Difference between Periodic and Perpetual Inventory System – Key Differences | Accounting Management

Periodic Inventory System

A periodic inventory system is an inventory system that records inventory levels at specific points in time.

These points in time are usually at the end of accounting periods. Periodic systems use physical count audits, where employees actually count each and every item in the store to get an accurate inventory level.

This amount is then compared to sales reports and purchase receipts to verify the amount of goods sold and to see if there are any discrepancies in numbers.

Perpetual Inventory System

On the other hand, a perpetual system is an inventory system that records inventory in the accounting system on a continuous basis. This type of system relies heavily on automation to instantly track purchases and sales, and update the accounting system immediately.

When an item is purchased, it is automatically recorded in the accounting system as an inventory item.

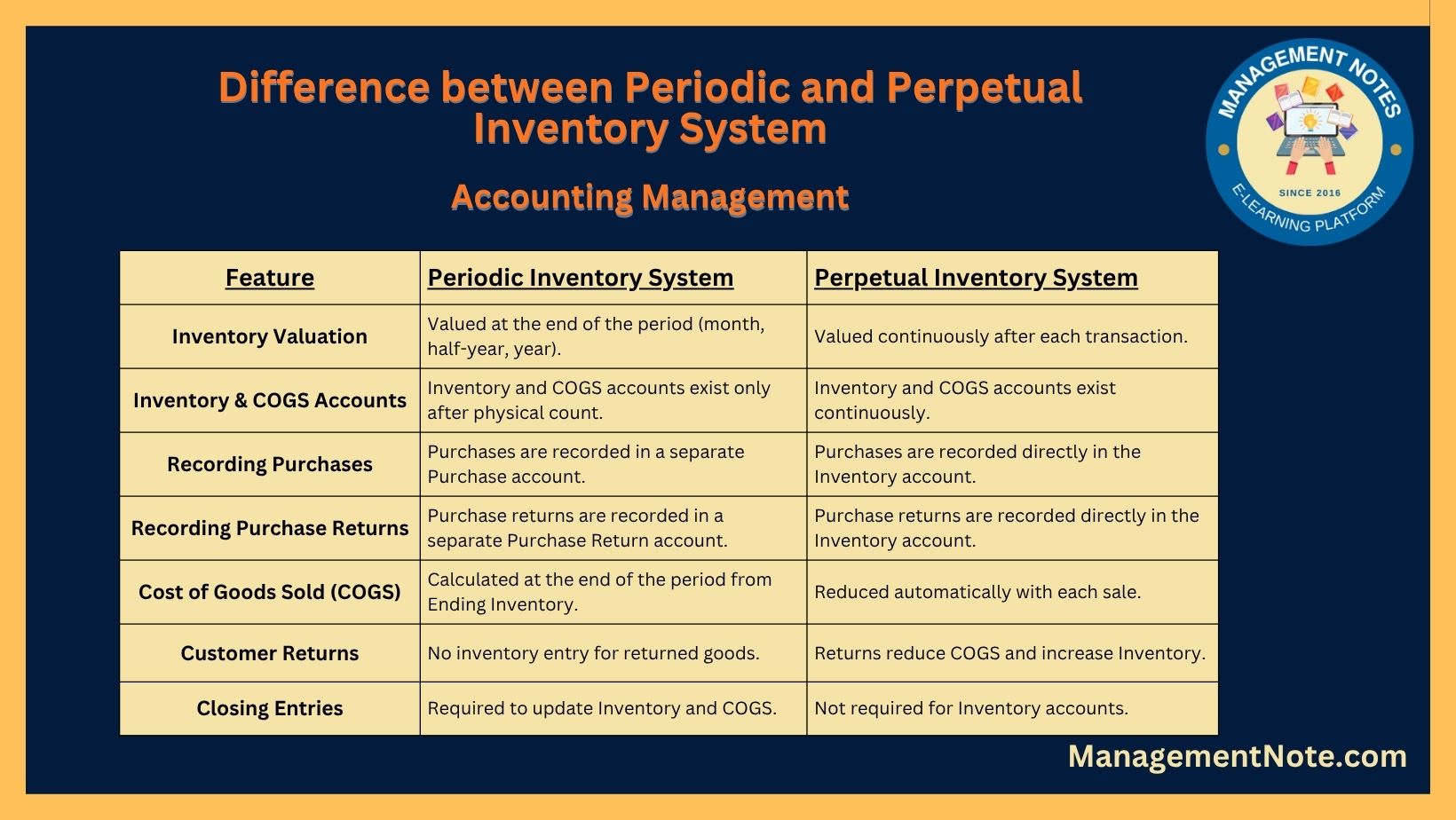

Difference between Periodic and Perpetual Inventory Systems

Periodic Inventory System |

Perpetual Inventory System |

| In periodic inventory, inventory is valued at the end of the period. That may be the end of the month, end of the half-year, end of the year, etc. | In a perpetual inventory system, inventory is valued after each and every transaction. |

| In this system inventory account and cost of goods sold are non-existent. until the physical count at the end of the year. | In this system account and balance of the costs of goods sold and inventory account exist all the time. |

| In this system purchase account is used to record purchases. | In this system, no individual purchases an account but the purchases are recorded in the inventory account. |

| In this system purchase return account is used to record purchase returns. | In this system no individual purchases account but recorded in the inventory account. |

| In this system Cost of goods sold or cost of sale is computed from the Ending Inventory. | In this system Cost of goods sold or the cost of sale is reduced when there is a sale. |

| In this system for goods returned by customers, there are no inventory entries. | In this system goods returned by customers are recorded by reducing the Cost of goods sold and adding back to inventories. |

| Closing Entries are only required in the periodic inventory system to update inventory and cost of goods sold. | The perpetual inventory system does not require closing entries for inventory accounts. |

Periodic and perpetual inventory systems are two methods used by businesses to track their inventory and manage their stock levels.

They differ in how they record and update inventory information, and each has its advantages and disadvantages.

Here’s a breakdown of the key differences between these two systems:

1) Recording of Transactions:

Periodic Inventory System:

In this system, inventory transactions are not recorded continuously. Instead, a business typically takes physical inventory counts at specific intervals, such as weekly, monthly, or annually.

The cost of goods sold (COGS) and inventory balance are determined periodically, usually after each physical count.

Perpetual Inventory System:

In a perpetual system, inventory transactions are recorded in real-time as they occur.

This means that every time a product is bought, sold, or returned, the system is updated immediately to reflect these changes in the inventory balance and COGS.

2) Accuracy and Timeliness:

Periodic Inventory System:

This system is less accurate and provides a less timely view of inventory levels because it relies on occasional physical counts.

There can be discrepancies between the recorded inventory balance and the actual stock on hand until the next physical count is conducted.

Perpetual Inventory System:

Perpetual systems offer greater accuracy and provide up-to-the-minute information about inventory levels.

This real-time tracking minimizes the risk of stockouts or overstocking and allows for better decision-making.

3. Cost of Goods Sold (COGS) Calculation:

Periodic Inventory System:

COGS is calculated periodically, usually at the end of a specific accounting period, by subtracting the beginning inventory (from the previous period) from the ending inventory (from the current period) and adding the cost of purchases made during the period.

Perpetual Inventory System:

COGS is calculated continuously and automatically with each sale. The system deducts the cost of the sold items from the inventory balance as soon as the sale is made.

4. Complexity and Software:

Periodic Inventory System:

This system is simpler and may not require specialized inventory management software. It is often used by smaller businesses with lower transaction volumes.

Perpetual Inventory System:

Perpetual systems are more complex and typically require dedicated inventory management software or integrated enterprise resource planning (ERP) systems.

They are favored by larger businesses with high transaction volumes and a need for real-time data.

5. Auditing and Control:

Periodic Inventory System:

Auditing can be more challenging as discrepancies between recorded and actual inventory levels may not be identified until the next physical count.

It may be easier for inventory shrinkage or theft to go unnoticed.

Perpetual Inventory System:

Auditing and control are generally easier because discrepancies are identified immediately. Any discrepancies can be investigated and addressed promptly.

In summary, the main difference between periodic and perpetual inventory systems is the timing and method of recording inventory transactions.

Periodic systems update inventory and COGS periodically, while perpetual systems do so continuously in real-time.

The choice between the two systems depends on factors such as the size of the business, transaction volume, and the need for real-time inventory information.

References

- bloomreach.com. (n.d.-b). Perpetual vs. Periodic Inventory Systems | Bloomreach. https://www.bloomreach.com/en/blog/2021/perpetual-inventory-system-vs.-periodic-inventory-system

- Inventory, C. F. (n.d.). Periodic vs Perpetual Inventory System: Definition, Differences, Advantages, and Disadvantages. Cash Flow Inventory. https://cashflowinventory.com/blog/periodic-inventory-system-vs-perpetual-inventory-system/

Related Posts

MBA,BBA.

I am Smirti Bam, an enthusiastic edu blogger with a passion for sharing insights into the dynamic world of business and management through this website.

I hold a MBA degree from Presidential Business School, Kathmandu, and a BBA degree with a specialization in Finance from Apex College,

- Inside the Stop Insider Trading Act : How Congress Plans to Reform Lawmaker Stock Trades | Investment News - July 22, 2026

- Scrip Dividend: Meaning, How It Works, Tax Rules, and Examples | Types of Dividend Decision - July 22, 2026

- Time Value of Money (TVM): Definition, Formula, Questions & Answers | Financial Management - July 22, 2026

Say, you got a nice blog post.Thanks Again.

Greetings! Very helpful advice in this particular article! It’s the little changes which will make the largest changes. Thanks for sharing!