Moving Average Inventory Method – Concept, Calculation, Advantages & Considerations | Accounting

Moving Average Inventory Method

In accounting, the moving average inventory method calculates costs of goods sold (COGS) and ending inventory values according to a cost flow assumption. Based on the cost of all units in inventory, including both old and new purchases, a weighted average cost per unit is calculated.

Calculation Process:

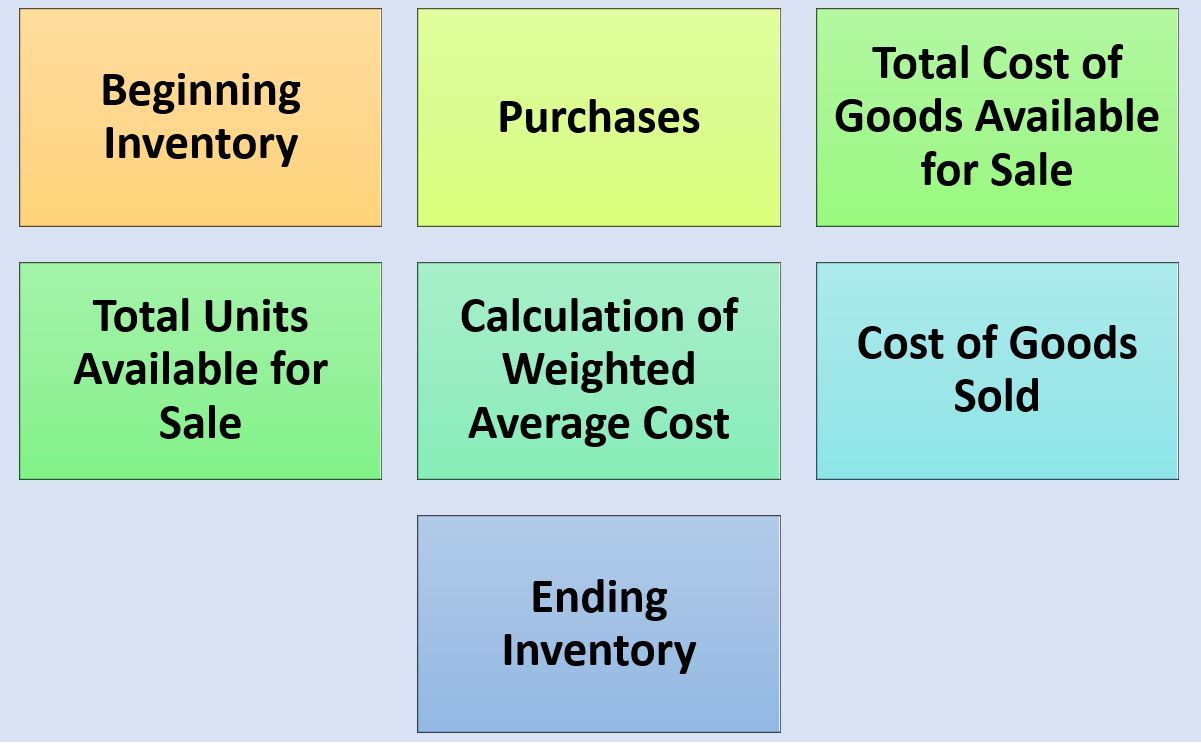

In the moving average inventory method, the average cost per unit is calculated by dividing the total cost of goods available for sale by the number of units available. Step by step, here’s how it works:

Beginning Inventory: In this calculation, the value and quantity of units in the beginning inventory are used. This can be a balance from the previous accounting period or the initial inventory for a new company.

Purchases: A new purchase’s cost and quantity are included in beginning inventory at the end of the accounting period.

Total cost of goods available for sale: In the total cost of goods available for sale, the cost of beginning inventory and new purchases is added together.

Total Units Available for Sale: It is the sum of the quantity of beginning inventory and the quantity of newly purchased units that is used to calculate the total units available for sale.

Calculation of weighted average cost: A weighted average cost per unit is determined by dividing the total cost of goods available for sale by the number of goods available for sale.

Cost of Goods Sold: A weighted average cost per unit is calculated by multiplying the quantity sold during the period by the cost of goods sold.

Ending Inventory: An ending inventory value is computed by multiplying the weighted average cost of each unit by the remaining number of units.

Advantages of Moving Average Inventory Method :

Some of the advantages of moving average inventory method are as follows:

Simplicity:

Moving average inventory is a relatively straightforward method compared to other cost flow assumptions, such as First-In-First-Out (FIFO) or Last-In-First-Out (LIFO). Based on the total cost of goods available for sale and the total number of units available for sale, a single average cost is calculated.

Smooths Cost Fluctuations:

In order to smooth out the effects of cost fluctuations, moving averages take the cost of both old and new purchases into account. For industries with volatile prices, it provides a more stable and predictable cost per unit.

Reflects Current Market Conditions:

A moving average method more accurately reflects current market conditions because it takes into account all items in inventory, including recent purchases. In industries where the cost of goods changes rapidly, this can be particularly useful.

Insulates from Seasonal Variations:

The moving average method can reduce the impact of seasonal variations in sales and purchases. In addition to including old and new purchases, it smooths out seasonal fluctuations, resulting in a more representative cost per unit throughout the year by accounting for them.

Streamlines Record-keeping:

By implementing the moving average method, businesses can simplify inventory valuation record-keeping. As a result of the method, businesses can maintain one average cost per unit instead of tracking each individual unit’s cost, reducing inventory management complexity.

Reduces the Risk of Obsolescence:

As the moving average method incorporates both old and new inventory prices, it ensures that older inventory is not undervalued when compared to newer inventory. By incorporating both old and new inventory prices, it reduces inventory obsolescence risk.

Reduces Distortion from Significant Price Changes:

Moving averages can provide a more reliable and stable cost basis in industries where prices fluctuate significantly, such as commodities or volatile markets. Using it can help reduce distortions resulting from abrupt price changes in the cost of goods sold and ending inventory.

Facilitates Cost Control and Pricing Decisions:

This information can be useful for cost control and pricing decisions since it provides companies with a better understanding of the average cost of their inventory.

In addition to evaluating profitability, assessing pricing strategies, and making informed decisions regarding inventory replenishment and production costs, it also enables businesses to evaluate profitability.

Considerations for Implementation:

Some of the considerations for implementing the moving average inventory method are as follows:

Consistency:

A consistent application of the moving average method is crucial to ensure accurate financial reporting. A change in cost flow assumptions between accounting periods can lead to distortions in financial statements and make comparisons more difficult.

Compatibility with Sales Pattern:

A moving average method may be more appropriate for businesses with relatively stable sales patterns. When sales fluctuate significantly or when there are seasonal variations, other cost flow assumptions like FIFO or LIFO may be more appropriate.

Impact on Profit Margins:

It is important to note that the moving average method can produce different profit margins as compared to other cost flow assumptions. Its profits are influenced by the timing and cost fluctuations of purchases.

Tax considerations:

Inventory costing methods, including the moving average method, can have significant tax implications. In order to understand the tax consequences and regulations related to inventory valuation and cost flow assumptions, businesses should consult with tax professionals.

Implementing and maintaining tracking systems:

Businesses may need to purchase inventory tracking systems that can accurately calculate and update moving average costs when they implement the moving average method. In addition to capturing the cost of each inventory purchase, these systems should also track the quantities of units sold.

Choosing to use the moving average method should be based on an assessment of the implementation and maintenance costs.

Compatibility with Inventory Management Systems:

A moving average method may need to be adjusted or integrated with existing inventory management systems if it is not compatible. In order to generate accurate reports based on the moving average cost calculation, businesses should ensure their inventory management software or systems are compatible.

Impact on Financial Ratios and Analysis:

Moving averages have a potential impact on financial ratios and analysis. Gross profit margin and inventory turnover can be affected by different inventory costing methods.

It is possible for stakeholders, such as investors and lenders, to have preferences or expectations about how inventory costing methods are chosen and how they influence financial performance.

Industry Standards and Regulatory Compliance:

Specific inventory costing methods may be required or preferred depending on the industry or regulatory requirements. A business should consider industry standards and regulations when choosing an inventory costing method. They may need to align with industry guidelines or ensure compliance with accounting regulations.

Moving average inventory is an accounting method that uses cost flow assumptions to figure out the cost of goods sold and the value of ending inventory. Moving average provides simplicity, smoothes cost fluctuations, and accurately reflects current market conditions by calculating a weighted average cost per unit based on all units in inventory.

It is, however, important to consider consistency, compatibility with sales patterns, impact on profit margins, and tax considerations when using the moving average method.

It is possible for businesses to track inventory costs accurately and make informed financial reporting, pricing, and profitability decisions by using this method appropriately.

I am Bijisha, an enthusiast with a profound eagerness for learning. I hold a Bachelor’s degree in Business Administration(BBA) from Apex College. I am constantly driven by a relentless curiosity and a genuine desire to expand my knowledge horizons.

- Top 10 Best Books for Hospitality Management - December 9, 2023

- Top 10 Best Sociology Books for Beginners - December 5, 2023

- Top 10 Best Psychology Books on Human Behavior - December 3, 2023