Objectives of Budgetary Control – Budgetary Control | Cost Accounting

Objectives of Budgetary Control

For every enterprise, budgetary control involves determining the actual results and comparing them with budgeted figures and standards for the future period.

The variance between budgeted figures and actual performance is then calculated. Prior to recording actual results, budgets are prepared.

There is a great deal of competition, uncertainty, and risk in the modern business world. As a result of the complexity of these management problems, a variety of managerial tools, techniques, and procedures have been developed that are useful for business management.

Among all the planning and controlling devices, budgeting is the most common, useful, and widely used.

In order to control costs and maximize profits, budgetary control has become an essential tool of management.

When the various factors of production are combined in a profitable manner, costs can be reduced, waste can be reduced, and income can be maximized.

What are the objectives of Budgetary Control?

Some of the objectives of Budgetary Control are as follows:

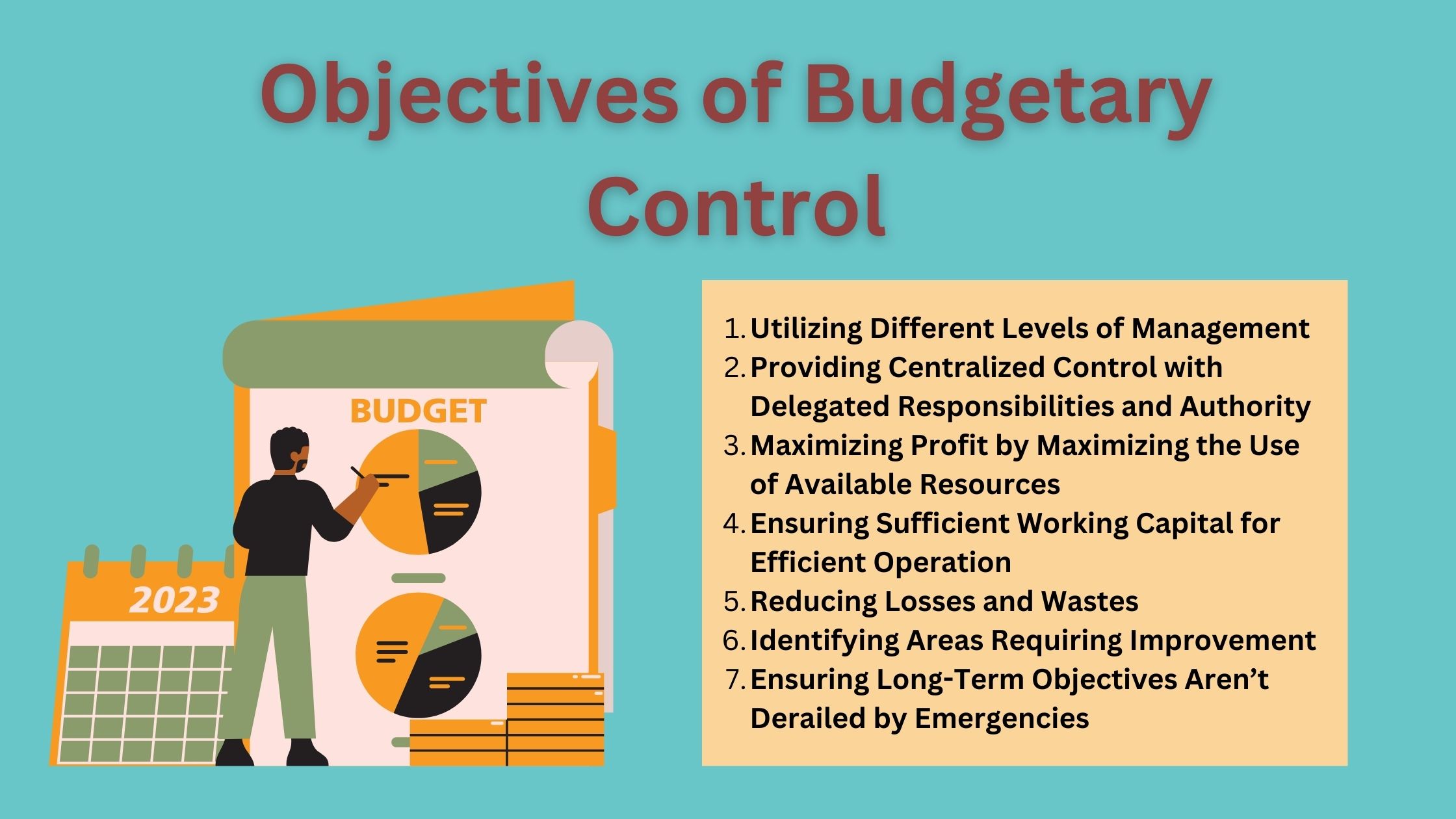

- Utilizing Different Levels of Management

- Providing Centralized Control with Delegated Responsibilities and Authority

- Maximizing Profit by Maximizing the Use of Available Resources

- Ensuring Sufficient Working Capital for Efficient Operation

- Reducing Losses and Wastes

- Identifying Areas Requiring Improvement:

- Ensuring Long-Term Objectives Aren’t Derailed by Emergencies

1. Utilizing Different Levels of Management:

➔ Budgetary control involves engaging various levels of management within a company to work together towards achieving the firm’s goals.

➔ This is like having a team where everyone has a specific role in achieving a common objective.

➔ By involving various management levels, budgetary control ensures that each tier contributes unique perspectives and skills.

|

Example: Think of a school project where students have different roles one is responsible for research, another for writing, and another for presentation. Each student plays a part, just as different levels of management contribute to achieving a company’s goals. |

2. Providing Centralized Control with Delegated Responsibilities and Authority:

➔ Budgetary control allows for central oversight while also empowering different departments or individuals with specific responsibilities and authority.

➔ It’s like having a captain steering a ship, but with crew members managing different aspects.

➔ This objective strikes a balance between central guidance and decentralized empowerment, akin to a symphony conductor directing musicians.

| Example:

In a soccer team, the coach provides overall guidance (centralized control), but players have specific roles and responsibilities on the field. The goalkeeper, for instance, is responsible for stopping goals. |

3. Maximizing Profit by Maximizing the Use of Available Resources:

➔ Budgetary control aims to ensure that a company makes the best use of its resources to maximize profits.

➔ It’s similar to using ingredients wisely in a recipe to create the most delicious dish.

➔ Budgetary control involves meticulous resource allocation, resembling a chef who optimally uses ingredients to create diverse and profitable dishes.

| Example:

Imagine a bakery using its ingredients efficiently – measuring flour accurately, not wasting eggs, and ensuring every resource contributes to making more cakes, ultimately maximizing profit. |

4. Ensuring Sufficient Working Capital for Efficient Operation:

➔ Budgetary control helps maintain adequate working capital, ensuring that a business runs smoothly.

➔ It’s akin to having enough fuel in a car to keep it moving without interruptions.

| Example:

Consider a delivery service. Proper budgeting ensures there’s enough money for fuel, maintenance, and unexpected expenses, allowing the delivery trucks to operate efficiently. |

5. Reducing Losses and Wastes:

➔ Budgetary control strives to minimize losses and wastes by careful planning and resource allocation, preventing unnecessary expenses.

➔ It’s like trying to finish a puzzle without losing any pieces.

| Example:

A manufacturing company can avoid losses by tracking the production process carefully, ensuring that raw materials are used efficiently and minimizing defects in the final product. |

6. Identifying Areas Requiring Improvement:

➔ Budgetary control helps pinpoint areas that need attention or improvement within a business.

➔ It’s like getting a report card that highlights subjects where you can do better.

➔ It highlights areas that need attention, enabling businesses to focus on improvement strategies and refine their operations.

| Example:

In a restaurant, if the budget reveals that food costs are high compared to revenue, management can focus on optimizing the menu and negotiating better deals with suppliers. |

7. Ensuring Long-Term Objectives Aren’t Derailed by Emergencies:

➔ Budgetary control safeguards a company’s long-term goals by planning for unforeseen events, preventing emergencies from derailing the overall strategy.

➔ It’s like having a backup plan to stay on course during a road trip.

| Example:

A tech company setting a long-term goal of launching a new product might allocate a portion of the budget for unforeseen challenges, ensuring that unexpected setbacks won’t hinder the overall objective. |

References

- Prajapati, A. (2019, September 28). Objectives of Budgetary control: 6 main objectives. Economics Discussion. https://www.economicsdiscussion.net/cost-accounting/objectives-of-budgetary-control/31915

Related Posts

MBA,BBA.

I am Smirti Bam, an enthusiastic edu blogger with a passion for sharing insights into the dynamic world of business and management through this website.

I hold a MBA degree from Presidential Business School, Kathmandu, and a BBA degree with a specialization in Finance from Apex College,

- Inside the Stop Insider Trading Act : How Congress Plans to Reform Lawmaker Stock Trades | Investment News - July 22, 2026

- Scrip Dividend: Meaning, How It Works, Tax Rules, and Examples | Types of Dividend Decision - July 22, 2026

- Time Value of Money (TVM): Definition, Formula, Questions & Answers | Financial Management - July 22, 2026