Capital Expenditure Vs. Revenue Expenditure – A Complete Guide for Businesses and Students | Accounting Management

Capital expenditure (CapEx) is money a business spends to buy or improve long-term assets. Revenue expenditure (RevEx) is money spent on day-to-day operations. Knowing the difference helps businesses make smarter financial decisions, file taxes correctly, and show investors a true picture of the company’s financial health.

What Is Capital Expenditure (CapEx)?

Capital expenditure, often shortened to CapEx, is money a business spends to buy, upgrade, or extend the life of a long-term asset. These are big-ticket purchases that help the company earn money over many years – not just this year.

The IRS and US accounting standards (GAAP – Generally Accepted Accounting Principles) require businesses to record CapEx as an asset on the balance sheet, then slowly expense it over time through depreciation or amortization.

What Counts as Capital Expenditure?

Capital expenditure typically includes:

- Purchase cost of the asset (minus any discounts received)

- Delivery and shipping costs

- Legal and closing fees (for example, costs to buy property)

- Installation costs (setting up a machine or software system)

- Upgrade costs that increase what the asset can do

- Replacement costs for major parts that extend useful life

The Golden Rule of CapEx

If the spending increases the asset’s earning capacity, extends its useful life, or adds a new capability, it is almost always a capital expenditure.

What Is Revenue Expenditure (RevEx)?

Revenue expenditure is money spent to run the business day-to-day. These costs keep the business going but do not increase the value or life of any asset. They are fully expensed in the same accounting period in which they occur – meaning they reduce profit right away.

What Counts as Revenue Expenditure?

- Repair and maintenance costs (fixing a broken machine to its original state)

- Utility bills (electricity, water, internet)

- Employee wages and salaries

- Office supplies (paper, pens, printer ink)

- Rent for office or warehouse space

- Insurance premiums

- Routine software subscriptions (monthly or annual SaaS tools)

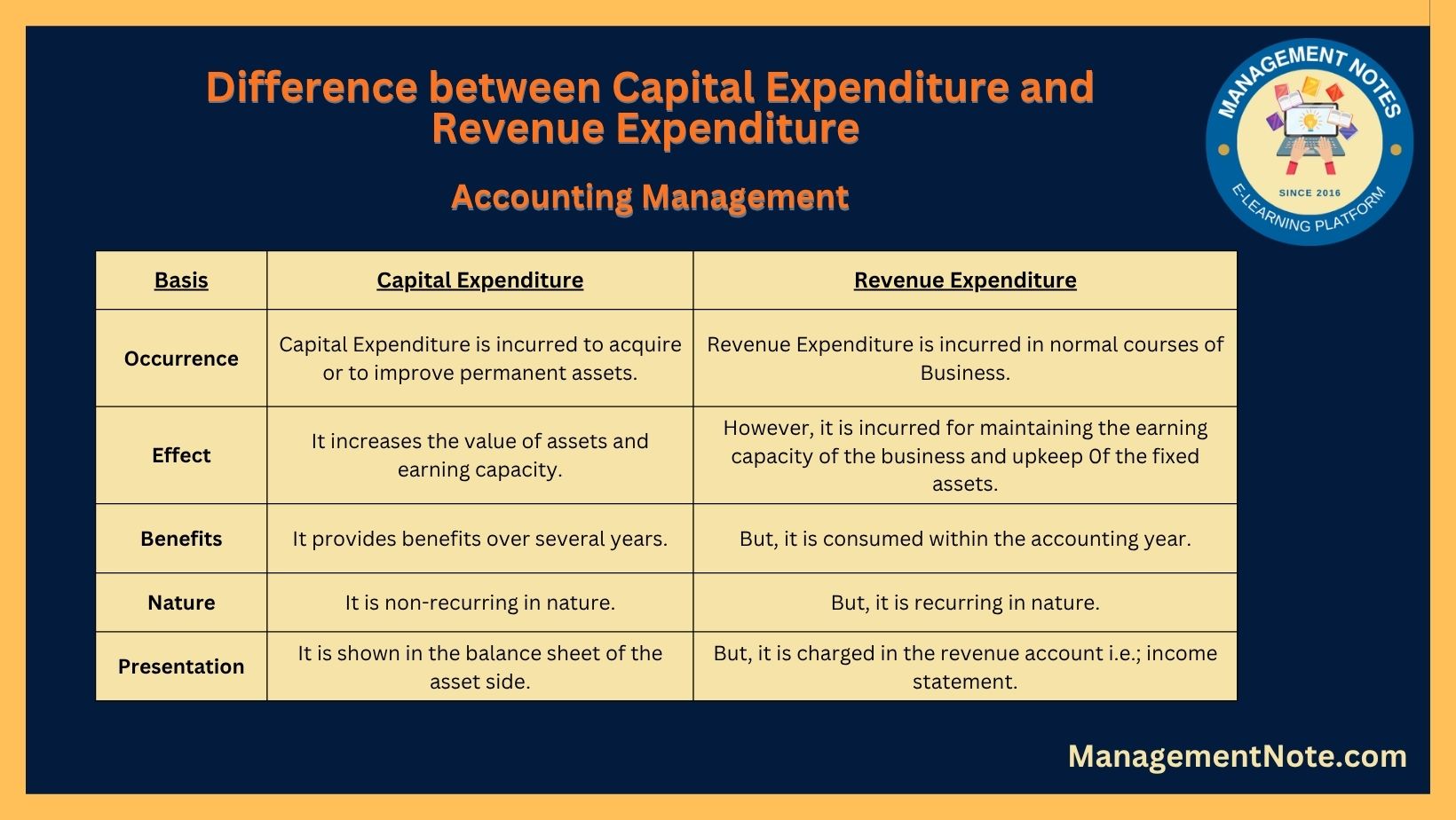

CapEx vs. RevEx: Key Differences at a Glance

The table below summarizes the most important differences between the two types of expenditure:

|

Basis of Comparison |

Capital Expenditure (CapEx) |

Revenue Expenditure (RevEx) |

|

Purpose |

Buy or improve long-term assets |

Maintain day-to-day business operations |

|

Effect on Assets |

Increases value or earning capacity of assets |

Maintains (does not increase) asset capacity |

|

Time Benefit |

Benefits spread over many years (multi-period) |

Benefits used up within the same accounting year |

|

Nature |

Non-recurring (happens occasionally) |

Recurring (happens regularly) |

|

Financial Statement |

Shown on the Balance Sheet as an asset |

Shown on the Income Statement as an expense |

|

Accounting Method |

Depreciated or amortized over useful life |

Fully expensed in the period incurred |

|

IRS Tax Treatment |

Deducted over time (depreciation schedule) |

Deducted in full in the year incurred |

|

Examples |

Buying a building, purchasing machinery, software development |

Electricity bills, routine repairs, salaries, rent |

Real-Life Examples from US Businesses

Let’s look at some everyday examples that show how this difference plays out in real American companies.

Example 1: Amazon Warehouse Expansion

Capital Expenditure: Amazon spends $500 million to build a new fulfillment center in Ohio. This is CapEx because the building is a long-term asset that will generate revenue for decades.

Revenue Expenditure: Amazon pays $50,000 a month to repair conveyor belts inside that same warehouse. Since the repairs only restore the belt to its original working condition, this is RevEx.

Example 2: A Local US Restaurant

Capital Expenditure: A restaurant in Chicago buys a new commercial oven for $20,000. The oven will be used for 10 years. This purchase goes on the balance sheet and is depreciated over its useful life.

Revenue Expenditure: The same restaurant pays $300 to fix a broken pilot light on that oven. Since it just restores the oven to working condition, it is a revenue expense recorded in full this year.

Example 3: A US Tech Company (Software Development)

Capital Expenditure: A software company spends $2 million developing a new app that will be sold for years. Under US GAAP (ASC 350-40), the development phase costs are capitalized as an intangible asset.

Revenue Expenditure: The same company pays $15,000 per month for cloud server hosting (AWS or Google Cloud). This is a regular operating expense – fully deducted each month.

Example 4: Ford Motor Company

Capital Expenditure: Ford spends $700 million to build a new electric vehicle factory in Michigan. This is CapEx – a major long-term investment that will generate revenue over many years.

Revenue Expenditure: Ford pays $2 million to repaint and clean its existing factory floors every year. This maintenance cost keeps the facility running but adds no new value – it is RevEx.

How Capital Expenditure and Revenue Expenditure Are Recorded in Financial Statements

Capital Expenditure on Financial Statements

- Balance Sheet: CapEx appears under “Property, Plant & Equipment” (PP&E) or “Intangible Assets.”

- Cash Flow Statement: CapEx is recorded under “Investing Activities” as a cash outflow.

- Income Statement: Only the annual depreciation expense appears – not the full purchase price.

Revenue Expenditure on Financial Statements

- Income Statement: RevEx is shown in full as an operating expense in the period it occurs.

- Balance Sheet: Does not appear directly (it reduces retained earnings through the income statement).

- Cash Flow Statement: Appears in “Operating Activities” as a cash outflow.

Accounting Journal Entry Examples

|

Transaction |

Debit |

Credit |

|

Buy a delivery truck for $60,000 (CapEx) |

Vehicles (Asset) $60,000 |

Cash / Accounts Payable $60,000 |

|

Annual depreciation on truck ($12,000/yr) |

Depreciation Expense $12,000 |

Accumulated Depreciation $12,000 |

|

Pay $500 to repair truck tires (RevEx) |

Repair Expense $500 |

Cash $500 |

|

Pay monthly rent of $3,000 (RevEx) |

Rent Expense $3,000 |

Cash $3,000 |

Why This Difference Matters for US Taxes (IRS Rules)

The IRS has specific rules about how businesses can deduct capital vs. revenue spending. Getting this wrong can lead to penalties or missed tax savings.

Revenue Expenditure: Immediate Full Deduction

Revenue expenses are fully deductible in the tax year they occur. This reduces your taxable income right away.

Capital Expenditure: Depreciation Over Time

By default, CapEx must be depreciated over the asset’s useful life using the IRS depreciation schedule (MACRS – Modified Accelerated Cost Recovery System).

Key IRS Tax Provisions to Know

|

IRS Rule |

What It Does |

Who Benefits Most |

|

Section 179 Deduction |

Lets small businesses deduct up to $1,160,000 of CapEx in the year of purchase (2023 limit) |

Small & mid-size US businesses |

|

Bonus Depreciation (100% in 2023, phasing down) |

Allows businesses to deduct a large portion of CapEx immediately instead of over years |

Growing businesses with large CapEx |

|

MACRS Depreciation |

Standard IRS schedule for depreciating assets over their class life (e.g., 5 years for computers) |

All US businesses with fixed assets |

|

De Minimis Safe Harbor (Rev. Proc. 2015-20) |

Expenses under $2,500 per item can be expensed immediately even if they would normally be CapEx |

Small businesses and startups |

Source: IRS Publication 946 – “How to Depreciate Property” (irs.gov)

CapEx vs. RevEx in Different US Industries

|

Industry |

Typical CapEx Examples |

Typical RevEx Examples |

|

Manufacturing |

New assembly line, factory building, CNC machines |

Machine oil, labor wages, repair parts |

|

Technology / SaaS |

Server infrastructure, software development, patents |

Monthly AWS/Azure fees, support staff salaries |

|

Healthcare / Hospitals |

MRI machines, hospital wings, surgical equipment |

Medical supplies, staff wages, utility bills |

|

Retail (e.g., Walmart, Target) |

New store construction, warehouse automation |

Electricity, cashier wages, store cleaning |

|

Real Estate |

Property purchase, renovation, new roof |

Property management fees, routine landscaping |

|

Transportation (e.g., FedEx, UPS) |

Fleet of delivery trucks, cargo planes |

Fuel, driver salaries, tire replacements |

Common Mistakes Businesses Make

These are the most common errors US businesses and accountants make when classifying expenditure:

Expensing CapEx as RevEx: Immediately writing off a major asset purchase overstates expenses and understates profit. The IRS may reclassify it and charge back taxes.

Capitalizing routine repairs: Recording a repair as CapEx inflates assets and understates current expenses – a red flag for auditors.

Ignoring the de minimis rule: Small businesses sometimes miss the $2,500 safe harbor and go through unnecessary capitalization steps for low-cost items.

Not tracking improvement vs. repair: Replacing a roof is CapEx; patching a leaking section is RevEx. The line matters a lot at tax time.

Misclassifying software costs: Under GAAP, the development phase of internal-use software is capitalized; the preliminary and post-implementation phases are expensed.

Capital Expenditure FAQs

Q: How should you record a capital expenditure?

A: A capital expenditure is recorded as an asset on the balance sheet. The journal entry debits the asset account (e.g., Equipment) and credits Cash or Accounts Payable. Over time, the asset is depreciated – reducing the asset’s book value and recording a depreciation expense on the income statement each period.

Q: Which of the following is an example of a capital expenditure?

A: Common examples include:

- Purchasing a new company vehicle

- Building a new office or manufacturing plant

- Buying machinery or equipment for production

- Acquiring a patent or trademark

- Major software development for internal use

Q: A capital expenditure results in a debit to which account?

A: A capital expenditure results in a debit to an asset account – such as Property, Plant & Equipment (PP&E), Vehicles, Equipment, or Intangible Assets – depending on what was purchased.

Q: Which of the following is NOT a capital expenditure?

A: Routine repair and maintenance costs are NOT capital expenditures. Neither are utilities, rent, salaries, or any recurring expense that does not increase the earning capacity of an asset.

Q: Another name for a capital expenditure is:

A: Capital expenditure is also called CapEx, capital investment, capital spending, or simply a fixed asset purchase. In some contexts, it may also be referred to as a long-term investment.

Q: Which of the following items should be accounted for as a capital expenditure?

|

Item |

CapEx or RevEx? |

Reason |

|

Buying a new printing machine for $25,000 |

CapEx |

Long-term asset that increases production capacity |

|

Paying $400 to fix a broken office chair |

RevEx |

Small repair that restores, not improves, the asset |

|

Adding a new production line to a factory |

CapEx |

Increases the factory’s earning capacity permanently |

|

Paying monthly electricity bills |

RevEx |

Recurring operating cost with short-term benefit |

|

Buying a company car for the CEO |

CapEx |

Long-term asset, depreciated over its useful life |

Revenue Expenditure FAQs

Q: An expenditure for which of the following items would be considered a revenue expenditure?

A: The following items are typically classified as revenue expenditure:

- Routine maintenance and servicing of equipment

- Monthly rent for office or retail space

- Employee wages and payroll taxes

- Advertising and marketing costs

- Utility bills (electricity, gas, water)

- Small repairs that do not extend useful asset life

Q: Which of the following would be considered a revenue expenditure?

A: Paying $1,200 to service a company delivery truck is a revenue expenditure. The servicing restores the truck to its normal working condition – it does not extend its life or increase its capacity. Compare this with buying new truck tires that extend the truck’s operational life by two years – that would lean toward CapEx.

References & Citations

The information in this article is drawn from the following authoritative US sources:

- IRS Publication 946 – How to Depreciate Property. Internal Revenue Service. https://www.irs.gov/publications/p946

- IRS Revenue Procedure 2015-20 – De Minimis Safe Harbor Election for Tangible Property. Internal Revenue Service.

- FASB Accounting Standards Codification (ASC) 360 – Property, Plant, and Equipment. Financial Accounting Standards Board. https://asc.fasb.org

- FASB ASC 350-40 – Intangibles: Internal-Use Software. Financial Accounting Standards Board.

- US GAAP (Generally Accepted Accounting Principles) – Conceptual Framework. FASB.

- Investopedia – Capital Expenditure (CapEx) Definition. https://www.investopedia.com/terms/c/capitalexpenditure.asp

- Corporate Finance Institute (CFI) – CapEx Guide. https://corporatefinanceinstitute.com/resources/accounting/capital-expenditure-guide/

- Amazon Annual Report 2023 – Capital Expenditure Disclosures. Amazon Investor Relations.

- Ford Motor Company 10-K Filing 2023 – SEC EDGAR. https://www.sec.gov/cgi-bin/browse-edgar

(Disclaimer: This article is for educational purposes only and does not constitute tax or legal advice. Always consult a licensed CPA or tax professional for advice specific to your business situation.)

Similarly, Other Related Posts:

MBA,BBA.

I am Smirti Bam, an enthusiastic edu blogger with a passion for sharing insights into the dynamic world of business and management through this website.

I hold a MBA degree from Presidential Business School, Kathmandu, and a BBA degree with a specialization in Finance from Apex College,

- Inside the Stop Insider Trading Act : How Congress Plans to Reform Lawmaker Stock Trades | Investment News - July 22, 2026

- Scrip Dividend: Meaning, How It Works, Tax Rules, and Examples | Types of Dividend Decision - July 22, 2026

- Time Value of Money (TVM): Definition, Formula, Questions & Answers | Financial Management - July 22, 2026

Hey there! I simply would like to give you a big thumbs up for your great information you’ve got right here on this post. I’ll be returning to your web site for more soon.

Normally I don’t learn article on blogs, but I wish to say that this write-up very pressured me to check out and do so! Your writing style has been surprised me. Thank you, very nice article.

Pingback: Importance of Capital Budgeting - Finance | Management Notes

Pingback: Difference between Financial Accounting and Management Accounting